In the first half of 2021, the center of international crude oil futures prices has moved up significantly, but it has shown a gradual upward trend. From January to April, European and American oil prices were under the dual support of production control and vaccination. , the oil price center moved steadily upward to consolidate around US$60/barrel, while the flattening of the epidemic curve in Europe and the United States and the peak season of fuel demand in the northern hemisphere summer provided an excellent window for market speculation, and European and American oil prices accelerated their rise and broke through. During this special historical cycle, crude oil seems to be not only the king of commodities, but also has the best half-year performance among major assets. This highlights the transformation of market investment logic under the rotation of cycles and breaks the long-term stock market trend. , bonds, and commodities investment sequence. Under the epidemic environment, multiple factors have jointly pushed oil prices to complete an epic V-shaped reversal. The Crude Oil Research Team of Zhongyu Information will elaborate on the important supporting points of oil price operation in the first half of the year and the details that may affect the future direction.

In terms of price data, Zhongyu Information monitoring data shows that as of the external market time of 6 On March 30, the U.S. crude oil WTI benchmark price closed at US$73.47/barrel, an increase of US$24.95/barrel, or 51.42%, from the end of 2020; the Brent benchmark price closed at US$75.13/barrel, an increase of US$23.33/barrel, or 45.04% from the end of 2020. %; WTI and Brent have not only recovered all the ground lost since the outbreak of the new crown epidemic, but have further risen to price highs since October 2018, only one step away from the red line of $80 in the traditional high oil price range. Benchmark oil prices in Europe and the United States recorded their fifth consecutive weekly rise and the largest half-year cycle increase in 12 years.

The epicenter of the global epidemic has shifted and the flattening of the epidemic curve in Europe and the United States supports the outlook for fuel demand

Since the breakthrough progress in vaccine research and development in the fourth quarter of 2020, vaccination in some areas around the world has The work has intensified and the world’s epicenter of the epidemic has gradually completed the transformation process from Europe and the United States to the Asia-Pacific and Latin America. During the recovery of oil prices, the Asia-Pacific consumer countries represented by China continue to maintain strong overbought operations, which is a major issue for the oil market. The return to balance has formed a key support. Although the procurement intensity in the Asia-Pacific region has declined due to the impact of the epidemic since the second quarter of 2021, the expectation of a strong recovery in demand triggered by the improvement of the epidemic prevention situation in Europe and the United States has injected impetus into the rise in oil prices in due course. The market generally believes that the expansion of fuel demand triggered by the economic recovery in Europe and the United States will cause demand to recover faster than supply expansion, which will cause more significant supply shortages in the future. The basis of all this is OPEC+’s protracted production control.

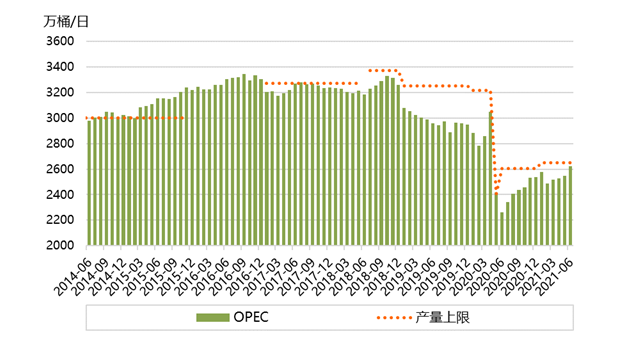

OPEC+’s protracted production control boosts the oil market

OPEC, a huge oil cartel, and its allies have shown unprecedented unity and consistency of action during the COVID-19 epidemic. OPEC has long been committed to safeguarding the interests of oil-producing countries. , many decisions are nothing more than a trade-off between long-term interests and short-term interests. In history, OPEC and its allies have used production adjustments to leverage the oil market countless times. This time, they seem to have achieved unprecedented success. OPEC+ has adopted long-lasting production restrictions and A more active market intervention mechanism has revived the oil market, although the collapse of the oil market may have been caused by OPEC itself. OPEC leader Saudi Arabia launched a price war to force Russia to submit. Of course, this may have led to its subsequent production cuts. During the negotiation process of the agreement, greater sacrifices had to be made to restore trust, but for OPEC+ and other oil-producing countries, the record production cuts undoubtedly reversed the market decline and greatly improved the financial situation of each producing country. This improvement is in line with multilateral interests, and from a practical point of view, the price paid by each oil-producing country is not as exaggerated as the benefits of the recovery in oil prices compared with the extent of the production reduction agreement, because the actual decline in demand itself will force crude oil-producing countries to reduce supply. quantity. As of June 2021, OPEC actually has only 5-6 million barrels per day of idle production capacity. However, as oil prices gradually rise back to a safe zone, the alliance of oil-producing countries is trying to absorb more dividends from rising oil prices by increasing production. On December 3, 2020, OPEC+ decided to slowly relax production restrictions starting in January 2021, replacing the previous coordination The scale of production reduction is slightly reduced from 7.7 million barrels per day to 7.2 million barrels per day, and monthly meetings will be held to adjust production policies at any time based on actual market developments. This actually further strengthens the intervention in the oil market and is lower than the expected increase in production. On the contrary, it stimulated market speculation, and the oil price center moved up widely at the beginning of 2021. OPEC+ still maintains restraint in increasing production despite the rapid recovery of oil prices. Its core demand is of course to hope that oil prices will rise further. Such unscrupulous promotion of price increases is precisely due to the sluggish recovery of the North American shale oil industry and the��The possibility is increasing because the supply gap will gradually be filled, and the strong recovery in demand hoped for by the market may not materialize as expected. ”

Although it was quite radical to make a judgment on the decline of crude oil prices during the period when crude oil was rapidly rising, the failure of many OPEC+ negotiations It seems that its internal differences will be difficult to bridge in the short term. The oil market is entering a period of expected revision. Oil producers and investment institutions are trying to convince the market that future oil demand growth will be stronger than foreseeable supply growth. However, potential supply growth Oil volume risks are increasing. Negotiations on the Iranian nuclear deal, which has long troubled the oil market since April, have been temporarily shelved, but the shadow of Iranian oil returning to the market lingers. The UAE has shown an attitude of not giving up until it achieves its goals this time. This short-term may be good for oil prices, but in the long run, it will mean that OPEC’s ability to control the oil market is weakened. However, the latest U.S. EIA inventory report shows that the benefits of the summer travel peak are being realized, and U.S. crude oil inventories and gasoline inventories are rising sharply. has declined, and fuel demand has even hit a historical record, which will help market bulls regain confidence and prevent oil prices from continuing to slide.

In the short term, oil prices can Does it have the potential to break through high oil prices or even reach around 100 US dollars? We think it is negative. Looking at the history of oil prices, ultra-high oil prices are often based on the expansion of geopolitical premiums, and the current oil market is more affected by financial The support of premium and supply and demand expectations lacks the necessary conditions for ultra-high oil prices. It is judged that the price centers of European and American crude oil in the third quarter of 2021 will be 74 and 75 US dollars/barrel respectively, and the price centers in the fourth quarter will be 68 and 70 US dollars/barrel respectively.

In the context of the epidemic, ideological opposition has become more acute, which has affected the global oil market structure. Relations between Russia and the European Union have become tense, and the EU is trying to gradually reduce its dependence on Russian energy supplies , according to market news, after EU sanctions, Glencore will not purchase any oil from Rosneft in July. It is expected that political confrontation will have a more concrete impact on the oil market, and Europe’s advanced energy transformation trend may Damage the long-term interests of traditional oil producers such as Russia, and the market share of Middle East oil producers led by Saudi Arabia in the Asia-Pacific market is also being weakened. Although this weakening is still within a controllable range, the Saudi-led alliance of oil producers refuses The call by major consuming countries represented by India to increase supply has prompted India and others to step up adjustments to their crude oil import structure, while crude oil from supplying countries such as the United States has become a fill-in part of the market share. This has actually pushed the benchmark price of WTI crude oil to be consistent with the Bren The price difference of special crude oil is further aligned.

China’s comprehensive tax control, environmental protection and inflation control policies have weakened the prospects for crude oil imports, and China’s decision-makers seem to have decided to completely squeeze out out of the hidden refined oil resources circulating in the market, and thoroughly regulate the import of crude oil and petroleum products. Blocking the import of diluted asphalt and other products may increase China’s local refining’s dependence on the share of crude oil imports, but the reduction of non-state trade quotas for crude oil It is possible that the refinery operating load will continue to decline, which is not conducive to the growth of crude oil demand in the long run. Another point is that China’s policymakers are committed to curbing the risk of rising inflation by curbing excessive speculation, despite seasonal demand. The rebound will support crude oil purchases, but excessive overbought operations will be suppressed, which means that crude oil imports will remain relatively low for a long time in the future, which is not good news for the forward oil market.

Also, now is certainly not the time to consider the theory of demand depletion, but the UAE’s attempt to sell as much crude as possible during a period of high demand reflects a sense of urgency that the Middle East The change in the production and sales policy of the country with the largest oil reserves reminds the oil market that on the one hand, OPEC+ can overcome barriers and cooperate closely in times of crisis, but when the market is functioning well, the differences that are covered up may have devastating results. The UAE and Saudi Arabia are both core members of the GCC and have long maintained close ties in political, religious, military and other aspects. However, the UAE has formulated ambitious oil expansion plans with international partners in recent years and launched a regional crude oil futures contract design with the intention of rapid expansion. To convert reserves into actual cash flow, it is imperative for the UAE to increase production. Even if it cannot increase production before the end of the agreement period in April next year, it will inevitably increase production quickly thereafter, which will still affect the supply and demand balance of the long-term oil market. .

The speed of energy transformation may accelerate under the epidemic environment. At present, some countries in the Western world have announced timetables for selling only fuel vehicles with net zero emissions. As the validity period of the established OPEC+ production reduction agreement is about to expire, the future output growth rate of traditional oil producing countries and emerging crude oil exporting countries such as the United States is likely to be faster than the growth rate of world oil demand. The possibility of future oversupply will drive down oil prices. Judging from the future 2~ The three-year European and American crude oil futures prices will be in the range of 60 to 70 US dollars per barrel, and there is still the possibility of testing the low oil price range again. It is expected that in the third quarter of 2021, oil prices will lock in the absolute high point of recent years, and then enter a long-term correction. In this period, the recovery of the world economy in 2022 will drive fuel demand back to pre-epidemic levels. However, the strong demand growth expected by the market is unlikely to become a reality based on China’s experience. It is expected that the European and American crude oil price centers in 2022 will be 65 and 67 US dollars respectively. / barrel, the European and American oil price centers in 2023 will be 60 and 63 US dollars / barrel respectively.

Can become a reality, it is expected that the European and American crude oil price centers will be 65 and 67 US dollars per barrel respectively in 2022, and the European and American oil price centers will be 60 and 63 US dollars per barrel respectively in 2023.

<br